In the 1960s, commercial aviation was booming.

And aircraft engine manufacturers wanted to take advantage of this new industry.

They had expertise and large production capacity coming from the Second World War.

Rolls-Royce was one of them.

But they were small compared with American giants like General Electric.

And how do you grow in this new industry when you don’t have an edge and have much less resources?

Rolls-Royce executives realized it’d be tough to beat others on price, speed, or efficiency.

But they also realized one key thing.

There was a big flaw in the business model for end customers.

They were selling engines to aircraft manufacturers like Boeing.

And those manufacturers sold aircraft to airlines.

So airlines became the owners of the engines once they purchased the aircraft.

Similar to what happens when we buy a car.

But this has created problems for airlines.

First, they had to pay unpredictable repair fees.

And if an engine became irreparable, that meant they had to buy a new engine.

They also lost additional money as they had to ground the aircraft during the maintenance.

And everybody knows airlines are low-margin businesses.

Hence every issue that affected their cash flow was critical.

What did Rolls-Royce do?

They let other engine manufacturers compete on price, efficiency, and speed.

They decided to solve the biggest problem for airlines.

How?

They offered a new program where airlines only had to pay a fixed fee per flight hour.

So regular engine maintenance?

Rolls-Royce handles it.

An unexpected repair?

No problem. Rolls-Royce got your back.

They called it Power by the Hour.

The program aligned the incentives of airlines and Rolls-Royce.

Airlines didn’t have to worry about unpredictable costs anymore.

And Rolls-Royce was incentivized to do predictive maintenance and build more reliable engines.

Airlines loved the program.

And they started buying more aircraft that had Rolls-Royce engines.

The program provided Rolls-Royce with long-term contracts with predictable revenue.

And they became a major player in a booming industry.

When brands ignore what the competition offers and innovate on value

We talked about Chan Kim and Renée Mauborgne’s Blue Ocean Strategy before.

One key aspect behind that idea is value innovation.

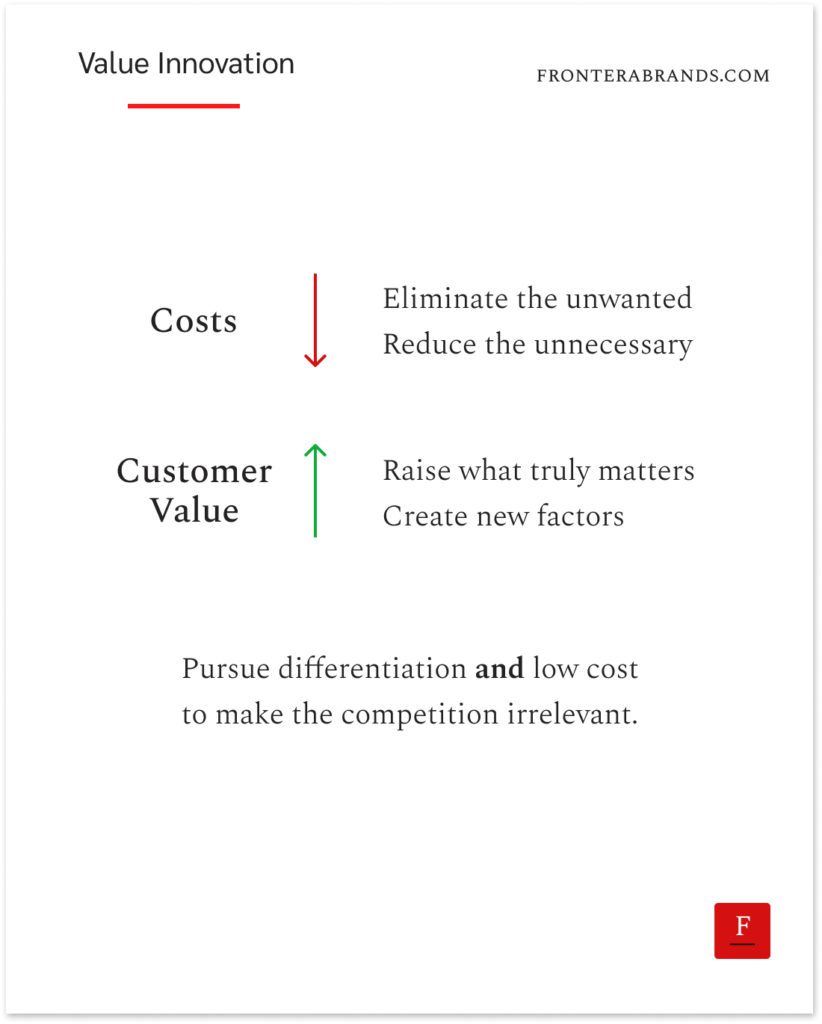

They say the belief that higher customer value can only come at a higher cost for the company is a fallacy.

So companies should chase differentiation and low cost at the same time.

And to do that you have to innovate on value.

How?

Well, many businesses compete on the same factors in mature markets.

And that makes competition fierce.

Everybody makes slightly better options for incremental gains.

Value innovation breaks that cycle.

You avoid competing on the same factors and change the game.

Like Rolls-Royce did.

They didn’t only focus on creating a cheaper, faster, or more efficient engine.

Another manufacturer would respond with an even cheaper, faster, or more efficient one.

They found a new value no other competitor offered.

And they created a long-term strategy to deliver it.

Competitors didn’t realize what was going on.

How could Rolls-Royce take on all the maintenance costs for a small fixed fee?

How could they even give up the revenue that comes from selling new engine parts to airlines?

It sounded stupid.

Sure, it was costly for Rolls-Royce in the short term.

But their strategy was to win in the long run.

So they exploited their new value which airlines loved.

After seeing its success, the rest imitated Rolls-Royce with similar programs.

But by that time Rolls-Royce had already gained its dominant position in the market.

So how can you innovate on value while reducing costs?

First, map out the key factors your industry competes on.

Price, features, benefits, risks…

You should end up with a list of at least ten.

45 Proven Frames to Differentiate Your Brand document I shared can help you list some.

Then go through the four steps Kim and Mauborgne gave.

Four steps to value innovation:

1. Eliminate the unwanted

“Which of the factors that our industry takes for granted should be eliminated?”

Every industry operates on certain assumptions.

And most businesses accept them without question.

But these “rules” are not immutable laws.

They can be challenged.

We talked about how ignoring “best practices” is a good way to differentiate.

So the first step to value innovation is finding what you can eliminate from these factors.

Some examples:

- Industry assumed unpredictable engine repair costs were inevitable for airlines. Rolls-Royce eliminated the risk of unexpected repair costs.

- Industry assumed all businesses had to host their CRMs on their own servers. Salesforce eliminated that need by providing a CRM in the cloud.

- Industry assumed intermediaries were part of the game to sell computers. Dell eliminated the dependence on middlemen by selling computers through phone and online orders.

2. Reduce the unnecessary

“Which factors should be reduced well below the industry’s standard?“

The next is finding the factors that increase costs for no gain.

So you can reduce them to achieve a cost advantage.

Some examples:

- Rolls-Royce reduced sporadic repairs (with predictive maintenance) and the cost per unit of maintenance with economies of scale. So they were able to offer long-term Power by the Hour contracts.

- Yellow Tail reduced the variety of wines by offering only two wines. So they reduced production costs drastically compared with other wine makers.

- Southwest reduced services provided on a flight and started using more distant airports. So they created low-cost flights where the main point was to take passengers from A to B.

3. Raise what truly matters

“Which factors should be raised well above the industry’s standard?”

Some factors are more important for customers than it seems.

When brands don’t provide them because of cost, it becomes a dealbreaker for customers.

So you find the value that truly matters at this step.

And you raise it above competitors.

Examples:

- Hotel chain Formule 1 increased the cleanness of rooms and bed comfort despite being low-cost. (They eliminated lobbies and 24/7 receptions which didn’t matter to most customers.)

- Salesforce increased the ease of implementing a CRM for SME sales teams.

- Yellow Tail increased the simplicity of choosing a wine with simple labels and wine selection.

4. Create new factors

“Which factors should be created that the industry has never offered?”

And this is the fun part.

How can you change the game by offering something new?

It seems hard to find an answer at first.

But the new value becomes obvious after going through the previous three steps:

- Rolls-Royce knew they had to eliminate the risk for airlines. So they invented the Power by the Hour model where airlines only had to pay for flight hours.

- Dell knew large inventory costs would kill the company. So they introduced a build-to-order model to reduce inventory costs. It also allowed businesses to order custom computers based on their needs.

- Amancio Ortega knew people would buy more clothes if there were more collections every season. So Zara invented fast fashion where consumers see a new collection every time they go to a store.

The moral of the story?

To differentiate your brand, you have to ignore what the competition does.

You have to invent new rules for the game.

It takes some courage.

And it takes some thinking beyond the short term.

But that’s how some brands win big while everybody else competes for little gains.

–

Enjoyed this article?

Then you’ll love the How Brands Win Newsletter.

Get the “5 Mental Models to Differentiate Your Business” guide when you join. It’s free.